The housing market announcements from Victoria’s Allan Government came thick and fast last week. For an apartment market analyst, it was like drinking from a fire hose, as layer upon layer of announcements rolled out daily.

Each day, Jacinta Allen took the stand to birth a series of new initiatives. All tactfully leaked to the public like a Taylor Swift set list. Here is the housing announcement family from last week.

– Monday’ child was Activity Centres

– Tuesday’s child was Stamp Duty Savings

– Wednesday’ child was Land Releases

– Thursday’s child was Townhouse Teasers

– Friday’s child was VBA skelter

– Saturday’s child was VCAT’s helper

– Sunday was a day or rest to figure out what it all meant.

What impact will it have?

The biggest barrier to any of these housing announcements turning into new homes, is the cost of building any type of new home remains prohibitively high. Especially apartment buildings.

Some of the announcements have no real market impact. Like the one we wrote about last week on the introduction of the Rental Dispute Resolution Victoria (RDRV). So, let’s focus on the four major announcements and review the impact of each.

1. Activity Centres

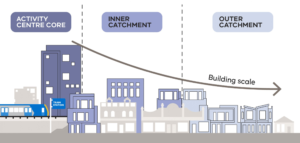

An Activity Centre is town planning jargon for an area around a transport node that allows higher density and mixed used development. It allows a mix of uses such as residential, commercial, retail, hospitality, health etc. Several areas of Melbourne like Box Hill, Doncaster and Frankston are already activity centres.

The announcement designated 25 of 50 new activity centres. Some are in tightly held neighbourhoods like Hawthorn, Toorak, Armadale, Brighton, and Sandringham.

Despite the planning changes, it is unlikely to spawn new development in these centres any time soon. Why is that?

Firstly, many sites or land holdings in these areas are too small to enable large development. It is possible adjoining owners may band together to create a larger site. This has happened previously in hot markets and rezoned areas where the combined land value of several sites, exceeds the collective individual improved value of each property.

The second reason new high rise apartment development is unlikely to kick off in the new activity centres, is that it is not financially viable. And won’t be for some time. The creation of an activity centre / planning change doesn’t change the numbers. Building apartment buildings is expensive.

As per our newsletter on 11 th September, Charter Keck Cramer (CKC) research shows apartment values need to rise by 15% to justify the cost of new apartment builds.

Activity centres however may encourage more medium density, higher end projects of 6 to 12 larger multimillion-dollar apartments. This doesn’t help the housing shortage as intended unfortunately.

2. Stamp Duty Changes

This announced a reduction in stamp duty for off the plan apartments and townhouses for just one year. It feels like the Black Friday Stamp Duty Sale. It is possible it is extended further it if the budget allows.

Previously a $620,000 off the plan apartment purchase would attract a stamp duty bill of $32,270. Now, off the plan apartments will incur stamp duty of about $4,000. (assuming the project has not started)

If we assume a $620,000 1-bedroom apartment is 50sq m ($12,400/sqm), then a $28,000 saving reduces the price by $560/sqm or 4.5%. Not enough to move the needle.

Remember CKC tell us prices need to increase by 15% to make apartment developments viable. This reduction in stamp duty (albeit helpful) will not flick the switch on new apartment projects either.

Domestic and foreign buyers both enjoyed stamp duty concession for off the plan apartments up until about 2017. That was scrapped by Labour and a surcharge for foreign buyers added. It knocked out the primary buyer cohort, and with it many apartment projects.

This was just one of the reasons the apartment development boom of the mid 2010’s ended, and the current housing shortage began. It is interesting to see the government turning back to stamp duty concessions for local buyers. Hopefully it becomes a permanent fixture.

3. Land Releases.

The planning process to develop land on Melbourne’s fringe has been notoriously frustrating for many years. Long and expensive planning processes including development of a Precinct Structure Plans (PSP’s) with adjoining owners which can take many years.

The detail on this recent initiative is unclear but the statement says 27 new greenfield areas will be given more certain timeframes. The focus is on the north-west (Melton, Caroline Springs, Beveridge) and south-east (Officer South, Devon Meadows, Cardinia Creek)

The catch here is the proposed overhaul to the developer contribution levy which could increase the tax payable by developers needed to develop this land. This cost (like all costs) will be passed through to home buyers if the development is to happen at all.

4. Backyard Townhouse

This is an extension of the “granny flat” rule that made it easier for people to build a second home on an existing block of land. It however extends it to allow subdivision of the two properties. The Allan government is considering a few options of how to allow this to happen so there is more to come here.

It will most likely cover dual occupancy (two homes on one title) and subdivision of an existing house block to enable two separately owned homes. The details including what size the block can be or what access and services it needs is not provided.

From a financial perspective the land value component for the owner zero (ie – they already own it) So it’s just the cost of construction including financing and risk that needs to be factored in. Subject to the details this should encourage new housing in appropriately sized and located house blocks.

Summary

From talking to developers and reading other people’s views, it seems last week’s housing announcements will have minimal short term impact on the inner suburban apartment market. The freeing up of land on Melbourne’s fringe is more likely to get traction in the short term and create housing subject to the cost and pricing of houses in each market. The market for existing house blocks on Melbourne’s fringe is flat. So just like apartments, the fringe housing market will need to pick up a lot to make new projects work.

Dual occupancy or building a second home on your existing block will be taken up quickly depending on the details of that initiative and construction costs.

The government is appropriately keen to leverage existing infrastructure in inner Melbourne with new apartments rather than build new infrastructure for new fringe housing. Unfortunately, this week’s announcement won’t make that happen yet.

Hi Recipient Name Greeting,

The housing market announcements from Victoria’s Allan Government came thick and fast last week. For an apartment market analyst, it was like drinking from a fire hose, as layer upon layer of announcements rolled out daily.

Every day, Jacinta Allen took the stand to birth a series of new initiatives. All tactfully leaked to the public like a Taylor Swift set list. Here is the housing announcement family from last week.

– Monday’ child was Activity Centres

– Tuesday’s child was Stamp Duty Savings

– Wednesday’ child was Land Releases

– Thursday’s child was Townhouse Teasers

– Friday’s child was VBA skelter

– Saturday’s child was VCAT’s helper

– Sunday was a day or rest to figure out what it all meant.

What impact will it have?

The biggest barrier to any of these housing announcements turning into new homes, is the cost of building any type of new home remains prohibitively high. Especially apartment buildings.

Some of the announcements have no real market impact. Like the one we wrote about last week on the introduction of the Rental Dispute Resolution Victoria (RDRV). So, let’s focus on the four major announcements and review the impact of each.

1. Activity Centres

An Activity Centre is town planning jargon for an area around a transport node that allows higher density and mixed used development. It allows a mix of uses such as residential, commercial, retail, hospitality, health etc. Several areas of Melbourne like Box Hill, Doncaster and Frankston are already activity centres.

The announcement designated 25 of 50 new activity centres. Some are in tightly held neighbourhoods like Hawthorn, Toorak, Armadale, Brighton, and Sandringham.

Despite the planning changes, it is unlikely to spawn new development in these centres any time soon. Why is that?

Firstly, many sites or land holdings in these areas are too small to enable large development. It is possible adjoining owners may band together to create a larger site. This has happened previously in hot markets and rezoned areas where the combined land value of several sites, exceeds the collective individual improved value of each property.

The second reason new high rise apartment development is unlikely to kick off in the new activity centres, is that it is not financially viable. And won’t be for some time. The creation of an activity centre / planning change doesn’t change the numbers. Building apartment buildings is expensive.

As per our newsletter on 11 th September, Charter Keck Cramer (CKC) research shows apartment values need to rise by 15% to justify the cost of new apartment builds.

Activity centres however may encourage more medium density, higher end projects of 6 to 10 larger multimillion-dollar apartments. This doesn’t help the housing shortage as intended unfortunately.

2. Stamp Duty Changes

This announced a reduction in stamp duty for off the plan apartments and townhouses for just one year. It feels like the Black Friday Stamp Duty Sale. While not part of the announcement it is possible it is extended further it if the budget allows.

Previously a $620,000 off the plan apartment purchase would attract a stamp duty bill of $32,270. Now off the plan apartments will incur stamp duty of about $4,000. (assuming the project has not started)

If we assume a $620,000 1-bedroom apartment is 50sq m ($12,400/sqm), then a $28,000 saving reduces the price by $560/sqm or 4.5%. Not enough to move the needle.

Remember CKC tell us prices need to increase by 15% to make apartment developments viable. This reduction in stamp duty (albeit helpful) will not flick the switch on new apartment projects either.

Domestic and foreign buyers both enjoyed stamp duty concession for off the plan apartments up until about 2017. That was scrapped by Labour and a surcharge for foreign buyers added. It knocked out the primary buyer cohort, and with it many apartment projects.

This was just one of the reasons the apartment development boom of the mid 2010’s ended, and the current housing shortage begin. It is interesting to see the government turning back to stamp duty concessions for local buyers. Hopefully it becomes a permanent fixture.

3. Land Releases.

The planning process to develop land on Melbourne’s fringe has been notoriously frustrating for many years. Long and expensive planning processes including development of a Precinct Structure Plans (PSP’s) with adjoining owners which can take many years.

The detail on this recent initiative is unclear but the statement says 27 new greenfield areas will be given more certain timeframes. The focus is on the north-west (Melton, Caroline Springs, Beveridge) and south-east (Officer South, Devon Meadows, Cardinia Creek)

The catch here is the proposed overhaul to the developer contribution levy which could increase the tax payable by developers needed to develop this land. This cost (like all costs) will be passed through to home buyers if the development is to happen at all.

4. Backyard Townhouse

This is an extension of the “granny flat” rule that made it easier for people to build a second home on an existing block of land. It however extends it to allow subdivision of the two properties. The Allan government is considering a few options of how to allow this to happen so there is more to come here.

It will most likely cover dual occupancy (two homes on one title) and subdivision of an existing house block to enable two separately owned homes. The details including what size the block can be or what access and services it needs is not provided.

From a financial perspective the land value component for the owner zero (ie – they already own it) So it’s just the cost of construction including financing and risk that needs to be factored in. Subject to the details this should encourage new housing in appropriately sized and located house blocks.

Summary

From talking to developers and reading other people’s views, it seems last week’s housing announcements will have minimal short term impact on the inner suburban apartment market. The freeing up of land on Melbourne’s fringe is more likely to get traction in the short term and create housing subject to the cost and pricing of houses in each market. The market for existing house blocks on Melbourne’s fringe is flat so just like apartments, the fringe housing market will need to pick up a lot to make new projects work.

Dual occupancy or building a second home on your existing block will be taken up quickly depending on the details of that initiative and construction costs.

The government is appropriately keen to leverage existing infrastructure in inner Melbourne with new apartments rather than build new infrastructure for new fringe housing. Unfortunately, this week’s announcement won’t make that happen yet.

New apartments and houses will be built when the gap closes between the total cost of construction and the end value of the finished homes.