Let’s do a 2025 Apartment Market Health Check to understand what is going on and what the growth path is for apartment values.

We have put the stethoscope on the 5 value drivers being:

- Job security / Wage growth / Health of employment market.

- The availability and cost of property debt.

- The number of apartments for sale (new or existing)

- Relative level of buyer demand / Net migration

- Cost of living / Strength of the household balance sheet.

By analysing each one, we can understand the likely direction and timing of the property market. Each one has been rated as:

✅ – Positive

🟠 – Moderate

❌ – Negative

1. Job security / Wage growth / Health of employment market. ✅

While Victoria’s employment market is OK now, it faces headwinds that need to be monitored in the coming months. If job security drops, so will the demand and price of housing.

Victoria’s employment market is showing signs of resilience amid a tricky economic landscape. According to the Australian Bureau of Statistics (ABS), the state’s unemployment was 4.4% in March 2025, slightly above the national average of 4.1%. Despite this uptick, employment has grown by 2.2% over the past year, surpassing the 20-year pre-pandemic average of 2.0%.

The participation rate in Victoria decreased marginally to 66.9% in March 2025, down from 67.0% in February. Full-time employment increased by 15,000 to 10,014,100 people, while part-time employment rose by 17,200 to 4,530,000 people.

2. The availability and cost of property debt. ✅

This is perhaps the shining light in the housing market. The cost of property debt is poised to ease over the next 1–2 years. Major banks are forecasting a series of interest rate cuts. The Reserve Bank of Australia (RBA) is expected to reduce the cash rate from its current 4.1% to as low as 2.6% by early 2026, according to NAB’s projections. A decline in rates will lower mortgage repayments and lift the amount buyers can borrow and therefore pay.

In response, lenders are already offering more competitive mortgage rates, particularly to new customers. However, existing mortgage holders need to proactively negotiate or refinance to benefit from these lower rates. The anticipated rate cuts are also expected to stimulate housing demand, and therefore price increases, especially in segments targeted by first-home buyer schemes.

3. The supply of apartments for sale (new or existing) ❌

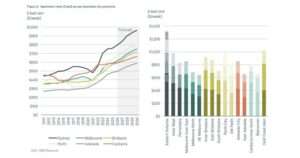

Unfortunately, the supply of apartments for sale (not new construction) is out stripping demand. Melbourne’s apartment market has seen a sharp rise in listings. Over the past year, the number of apartments for sale in the CBD has surged by 357% compared to the five-year average. This is largely due to investors offloading properties in response to rising holding costs and regulatory changes. Non-CBD listings volumes have been more stable but there is a ripple effect.

Fortunately for the market, new apartment construction remains historically low. In 2024, only 1,400 new apartments were completed in Inner-City Melbourne, marking the third-lowest annual level in two decades. The trend continues into 2025, with just 400 completions recorded in the first quarter, setting the stage for the lowest annual supply since 2008.

Looking ahead, while there are 22,000 apartments approved for development, the majority are in the build-to-rent sector, suggesting that the number of apartments available for purchase will remain low. This combination of increased resale listings and limited new supply presents a unique window for buyers seeking opportunities in Melbourne’s apartment market.

4. Relative level of buyer demand. 🟠

While net migration into Melbourne is strong, buyers remain cautious, and investors are taking some time to come out of hibernation.

Victoria’s population is experiencing a significant surge, primarily driven by overseas migration. In the year ending March 2024, the state added approximately 184,000 residents, marking a 2.7% annual growth rate. This was the highest of all Australian states. Notably, 84% of this growth stemmed from net overseas migration, with a large amount being temporary migrants, such as international students.

This influx has intensified rental demand in Melbourne’s apartment market, particularly in inner-city areas. Many migrants, especially those from Asian countries, exhibit a preference for apartment living due to cultural familiarity and proximity to urban amenities. Consequently, rental vacancy rates have plummeted, reaching 1.3% in May 2024, significantly below the long-term average of 2.6%. This scarcity has propelled median weekly rents upward by 4.8% over the past year and 16.4% over the past three years. This rise in rents is making investors sit up and look.

Ref Urbis

Looking ahead, the apartment market is expected to remain attractive to owner-occupiers, especially first-home buyers, due to continued affordability and lifestyle considerations. Investor activity will remain subdued unless policy adjustments remove the current disincentives. (don’t hold your breath)

5. Cost of living / Household balance sheet.❌

If a drop in interest rates is the market’s shining light, the cost of living is the market’s blight.

As the cost-of-living bites harder across Victoria, its ripple effects are becoming increasingly evident in Melbourne’s broader market, particularly among younger, urban-focused buyers.

It has made it harder to save a deposit and pay a mortgage. Especially for first-home buyers and downsizers or retirees who traditionally dominate the apartment market. First-home buyers, face mounting challenges of stagnant wage growth and increased essential costs. This erodes their borrowing capacity.

These buyers chase affordability in smaller, more centrally located dwellings which is normally good for the apartment market. Many downsizers, feeling the financial squeeze of rising utility costs and taxes, are hesitant to sell and move, further restricting the flow of apartment stock.

The impact is twofold: demand for lower-priced, well-located apartments is strong but price sensitivity is higher than ever. This is pushing buyers to reconsider not just where they buy, but what compromises they’re willing to make on size, amenities, and strata fees. Cost-of-living pressures are reshaping buyer expectations, and the market must adapt.

Ref – Anyone’s credit card statement

Summary

We need the cost of living (relative to wages) to rebalance before any meaningful growth in apartment values occurs. Interest rates are part of that equation and a cut in rates will definitely help cash flow and confidence levels.

The sustained population growth, coupled with a lagging apartment supply pipeline, suggests upward pressure on the apartment market over a more extended period.