It looks like apartments are the big winner from the Federal Government’s upgraded First Homebuyer Guarantee Scheme. Even the Federal Government agrees that changes announced last week to The First Homebuyer Guarantee (buyer deposit scheme) will push up home prices.

The scheme per se is not new. What is new is the removal of the cap on how many people can use it, the increased value cap and complete removal of any income criteria. So Mike Cannon-Brookes children could put out their hand for government assistance to buy their first home. They just need to limit their budget to $950,000 (Melb)… unlikely 😄

The introduction of the scheme has also been brought forward to October 2025 from the previous timing of Jan 2026 as per the election promised schedule. Buyers opting into this scheme will avoid lenders mortgage insurance which applies to loans over 80% of the property value.

Unlike state based Help to Buy Schemes, it doesn’t advance the buyer any money or partner with them in the ownership. It simply guarantees up to 15% of the loan. This coupled with the buyer’s 5% makes the loan 20% “secured”. This ensures the participating lender is happy.

The buyer however is still borrowing 95% of the property value and is liable to repay it in full. Is that something that should be encouraged? If it gets people into ownership sooner and they satisfy the normal bank lending risk requirements then maybe it’s a good pathway. The normal way of saving the equity first doesn’t seem to be working.

For the housing market generally, it is a sugar hit and not a fix.

It enables people who have only saved 5% of the usual 10% to 20% equity to buy now. This potentially brings forward about 5-8 years of future buyers. It increases demand which pushes prices up.

The Government’s own treasury modelling shows it will push up housing prices by an extra half a percent over six years. Many experts say it will be a lot more than that.

Diana Mousina – Deputy Chief Economist at AMP, told ABC it will push up prices by an additional 3% over six years. This is in addition 0.5% p.a. on top of the expected 4% to 5% per annum market growth in housing prices.

Louis Christopher – SQM, said the scheme could result in an increase of 15% over six years on top of the normal market gains.

Falling interest rates are also starting to fuel buyer demand. We are expecting a further cut to the cash rate in September or November this year. These two factors plus a general lift in buyer sentiment should ensure a more buoyant market through ’25 – ’26.

While there is no cap on how many people can participate, there is a cap on the property value. This cap has been lifted from the old limit. These are the new proposed amounts.

| Capital City | New Cap | Old Cap |

| Adelaide | $900,000 | $600,000 |

| Brisbane | $1,000,000 | $700,000 |

| Canberra | $1,000,000 | $750,000 |

| Darwin | $600,000 | $600,000 |

| Melbourne | $950,000 | $800,000 |

| Perth | $850,000 | $600,000 |

| Sydney | $1,500,000 | $900,000 |

These caps vary in regional areas of each state.

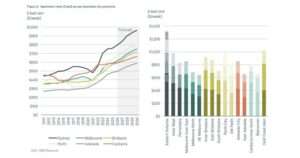

The apartment market will be the biggest beneficiary of this scheme. According to the Real Estate Institute of Victoria, the median house price in Melbourne is $924,000. The median unit (apartment) price is $635,000.

Pretty soon the median house price in Melbourne will top $1,000,000 meaning buyers will need to look for cheaper property to enjoy the government support this scheme offers. The median apartment price could jump 50% before it hits the upper limit of the eligibility value in Melbourne, so it has lots of headroom.

Apartment buyers are also often first home buyers which is a criterion of the scheme.

So, with the two key criteria of value cap and first home buyer satisfied by apartments, expect to see apartment buyers a frequent flyer of the First Homebuyer Guarantee. Buckle up.